Sept. 10: This story has been corrected.

Green Mountain Coffee Roasters’ first-ever investor day is Tuesday, and the company is flying high.

The stock price of the company, which sells coffee machines under the Keurig brand and the little K-Cups that go in them, has soared more than 260 percent in the last year.

Despite persistent questions, most of Wall Street remains resolutely bullish on Green Mountain, which has a market value of $12 billion.

In 2010, the company disclosed it was being investigated by the Securities and Exchange Commission. In 2011, the hedge fund manager David Einhorn, who is betting against Green Mountain’s stock price, delivered a highly critical 110-slide speech at an investor conference, raising questions about the company’s future prospects and, more seriously, its bookkeeping. He followed up a year later with another one.

A class-action lawsuit, which was dismissed, quoted anonymous former employees about suspicious activities. Green Mountain has said it conducted an internal investigation that cleared the company.

Green Mountain operates on a razor/razor blade model — selling brewing machines but making its real money on the K-Cups. It used to disclose exactly how many K-Cups it sold but stopped doing so in 2010. Instead, it tells investors the year-over-year percentage growth. Wall Street has dutifully plugged numbers in to estimate the unit sales.

Last year, Green Mountain faced expirations of the patents that covered its brewing system. Wall Street has been monitoring whether Green Mountain will lose market share to new private-label knockoffs. And indeed, a recent Barron’s article suggested that it was losing share faster than expected.

A recent disclosure from the company’s new chief executive, Brian Kelley, has revived the questions about sales, as do on-the-ground accounts I have received from former factory and warehouse workers.

Because Green Mountain’s investor day will give analysts and shareholders unusual access to company executives, it seems like an opportunity to ask them some hard questions.

Here are a few from me.

Just how many K-Cups has Green Mountain sold year-to-date and is it less than the Street understands?

Going by the average of six analysts’ estimates, Green Mountain should have sold roughly 6.9 billion K-Cups over that time period. But that’s “in the neighborhood of 10 percent” too high, says an outside spokesman for Green Mountain, Darren Brandt, of Sloane & Company.

That puts the K-Cup sales volume at around 6.2 billion. The company says it isn’t surprised there is a wide range of Wall Street estimates because it doesn’t disclose the figure. (To be fair, the Canaccord analyst is pretty close, estimating 6.3 billion. The Longbow and Lazard Capital Markets analysts are far too high, with Longbow projecting 7.3 billion, and Lazard Capital 7.7 billion.)

How wide is the gap between how many K-Cups the company says it has sold and how many have ended up in customer’s hands? And why?

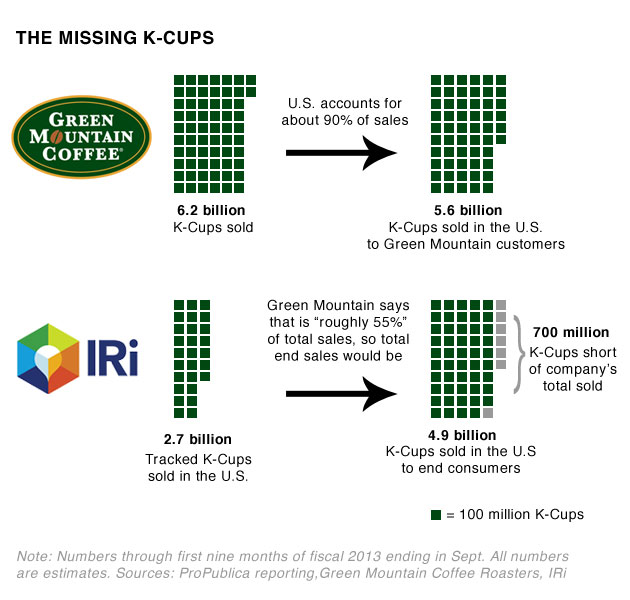

During the company’s third-quarter earnings conference call on Aug. 7, Mr. Kelley disclosed that IRI, a consumer products data tracker, captures “roughly 55 percent” of the company’s K-Cup sales volume in the United States.

IRI tracks sales at some retailers like Bed Bath & Beyond, but not at others, like Costco. It also doesn’t capture things like direct sales to offices (ProPublica’s Keurig machine gets plenty of use).

Roughly 90 percent of Green Mountain’s K-Cup sales are in the United States, based on company disclosures. Using the company’s math, that would add up to 5.6 billion in K-Cup sales so far this year.

IRI, however, has tracked only about 2.6 billion K-Cup sales for the first nine months of the year, according to an analysis I was furnished with. If, as Mr. Kelley says, that 2.6 billion represents 55 percent of the total, then 100 percent would be about 4.7 billion.

That’s a far cry from 5.6 billion. There seems to be a gap in the United States of about 900 million K-Cups.

What’s going on?

Mr. Brandt said the company declined to give its overall sales volume, but said the IRI number that I was furnished with was too low. He said a company analysis indicated that this portion of Green Mountain’s sales should be about 2.7 billion, not 2.6 billion.

Still, even if we use the company’s figure of 2.7 billion, total sales in the United States would be 4.9 billion, or about 700 million K-Cups short of what the company has said. That’s a lot of extra K-Cups sitting in the channel.

Mr. Brandt said that for companies like Green Mountain it was perfectly ordinary for there to be a difference between sales to its customers and end sales to consumers, as tracked by IRI.

What explains the unusual movements of Green Mountain inventory described by some former company workers and associates?

I spoke to Tim Jackson, 43, who worked for Green Mountain in its Knoxville, Tenn., facility as a material handler and in the shipping department from August 2009 to August 2011.

He acknowledges that he was dismissed for not getting to work reliably. But he said Green Mountain moved its inventory in ways he found strange.

“A lot of things seemed kind of hinky,” he said. “Inventory levels were pushed to extremes and then they transferred them around from one sister company to the next.”

He added: “These are finished products, finished cartons, ready for the shelves. Why transfer the product? Why not sell it straight from here? Why pay for the shipping?”

Sometimes, he said, he would see the same pallet of boxes come back to the Knoxville facility. Mr. Jackson said he had worked in similar facilities at other companies and hadn’t seen that before.

Mr. Jackson said such transfers were “more predominant before inventory audit.”

Frank DeStefano, 32, worked as a production planning manager for M. Block and Sons, which handles Green Mountain’s warehousing and logistics in Bedford, Ill. He worked there about seven months and said that after he started asking questions, he was let go in March 2011.

M. Block did not respond to a request for comment.

Though he worked for M. Block, he said, “I was told by Keurig what to do with everything.”

He echoed Mr. Jackson’s account. “As far as the coffee went,” he said, “it wasn’t moving as quick, always being transferred from one warehouse to another warehouse.”

Mr. DeStefano said that on two occasions, before an audit, Green Mountain filled large orders from QVC, the home shopping channel. “We would shove it all inside trucks and ship a bunch to QVC. After the audit was done, more than half was sent back.”

QVC did not respond to a request for comment.

“They would say just buyer’s remorse,” he said. “That seems kind of strange that half of those would come back.”

A company spokeswoman said that any movements between company units and with third-party logistics companies were not booked as sales and that the company adheres to proper revenue recognition rules.

“These allegations from former employees are unfounded,” a company spokeswoman said in a statement. “The allegations surrounding suspicious sales of brewers to QVC prior to an audit were first raised in a complaint filed in the litigation. As we responded, they are so logistically implausible that one cannot conclude that the source’s statements are reliable.”

The company said it was cleared by an internal investigation. And the United States District Court in Vermont dismissed the class-action suit with prejudice, ruling that there was no evidence that suggested knowledge of the allegations by the top executives.

What is happening with the S.E.C.’s investigation of Green Mountain, which the company has said involves its accounting practices?

The company’s latest quarterly filing says the inquiry continues.

The new head of the S.E.C., Mary Jo White, has said publicly that one of her main goals is to put more resources into fighting accounting fraud. Keeping an investigation over a company’s head for years is unfair for everyone involved. Resolving the long investigation into Green Mountain one way or the other would do a great service for the investing public.

Not to mention caffeine lovers.

Correction (9/10): An earlier version of this column misidentified one of the Wall Street firms that published estimates of sales of Green Mountain's K-Cups. It is Lazard Capital Markets, not Lazard. (Lazard Capital split off from Lazard in 2005 as part of its former parent's initial public offering.)